With the work of the honey bee as our theme, we provide you with buzz on plan membership, investment results, and more! We hope you find the information interesting and relevant and we always welcome your feedback.

This report was prepared for plan members and participating employers as part of ELCIC Group Services Inc.’s ongoing strategic review and as a response to the 2021 Eastern Synod Assembly motion:

That the Eastern Synod petitioned Group Services Inc. to prepare a report detailing the advantages and disadvantages of the ELCIC joining a public sector type defined benefit pension plan and to make the report available to ELCIC congregations and GSI pension plan members.

We trust that this report provides useful information and an appreciation of the complexities around this issue and assessing other options. We will begin with a general governance framework and then get to more details.

2022 Q1 Investment Commentary ELCIC Pension Plan

There were several adverse factors influencing the investment markets in the first quarter of 2022. So, we are not surprised to see the disappointing results shown in this table. Most of us have likely noticed many of these influences in our everyday lives, including higher prices for fuel, difficulty getting goods and services, a lot of help wanted signs, and a housing boom. The events in Ukraine have given rise to a humanitarian crisis and a rippling effect on global economies. Inflation was also a major force as it climbed to the highest level in decades.

| ELCIC Pension Plan Investment Return

Jan 1 to Mar 31, 2022 |

Median Balanced Pension Plan as a comparison

Jan 1 to Mar 31, 2022 |

Excess return |

| -5.8 | -3.9 | -1.9 |

*Please note that information is not intended to be investment advice or to be a recommendation for your personal investment portfolio.

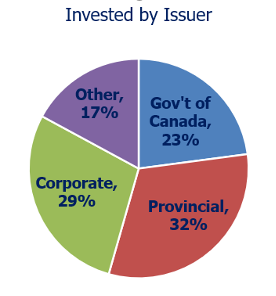

Growth Fund

Fixed Income

In case you missed this...

Twenty years ago, the need to provide members with timely and relevant information on changes and reminders to the Plans grew, and the “what’s News at GSI” newsletter was born. Since then, GSI has been consistently evolving and focusing on integrating financial wellness wherever possible. This Pension issue marks the first under the new name, “Your Plan Notes.” GSI chose this name to signify that the newsletter is about you, the plan member, learning about your Pension Plans, and creating plans for your retirement.

You may have heard about a phenomenon called languishing—an aimless, joyless state somewhere between depression and flourishing.

A New York Times article in April 2021 helped start a trend of discussion around languishing, describing it as a “sense of stagnation and emptiness” that many people seemed to be experiencing as part of the “emotional long-haul” of the COVID-19 pandemic.

But is languishing a real health condition? How might it appear in your life, or in the life of a loved one? And if it does, what can you do about it?

Have a question for GSI?